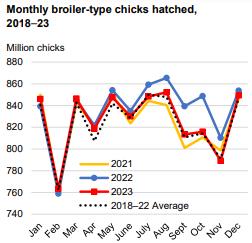

Broiler Chick Placements.

According to the February 21st 2024 USDA Broiler Hatchery Reports, 966.66 million eggs were set over five weeks extending from the week ending January 20th 2024 through February 17th 2024 inclusive. This quantity was higher by one percent compared to the corresponding period in 2023.

Total chick placements for the U.S. over the five-week period amounted to 927.85 million chicks. Claimed hatchability for the period averaged 79.5 percent for eggs set three weeks earlier, down from 79.8 percent for the preceding four-week period. Each 1.0 percent change in hatchability represents approximately 1.85 million chicks placed per week and 1.76 million broilers processed, assuming five percent culls and mortality with the current range of weekly settings.

Cumulative chick placements for the period January 7th through December 30th 2023 amounted to 9.67 billion chicks. For January 6th through February 17th 2024 chick placements attained 1.3 billion

According to the February 26th 2024 edition of USDA Chickens and Eggs pullet breeder chicks hatched and intended for U.S. placement during January 2024 amounted to 7.28 million, down 9.1 percent (226,000 pullet chicks) from January 2023 and 2.37 million pullet chicks or 24.5 percent less than the previous month of December 2023. Broiler breeder hen complement attained 61.2 million on February 1st 2024, 0.4 percent higher (300,000 hens) than on February 1st 2023.

Broiler Production

As documented in the February 23rd 2024 USDA Broiler Market News Reports for the processing week ending February 17th 2024, 164.2 million broilers were processed at 6.46 lbs. live. This was 4.8 percent less than the 172.8 million broilers processed during the corresponding week in the previous month of January 2024 and 1.9 percent less than the 167.4 million processed during the corresponding week in February 2023. Broilers processed in 2024 to date amounted to 1,123 million, 3.6 percent lower than for the corresponding period in 2023.

Ready to cook (RTC) weight for the most recent week was 806.1 million lbs. (366,399 metric tons). This was 6.5 percent less than the 861.8 million lbs. processed during the corresponding week in January 2024 and 3.1 percent less than the 809.0 million lbs. during the corresponding week in February 2023. Dressing percentage was a nominal 76.0 percent. For 2024 to date RTC broiler production attained 5,543 million lbs. (2.52 million metric tons). This quantity was 1.8 percent less than the corresponding period in 2023.

Broiler Prices

The USDA National Composite Weighted Wholesale price compared over a four-week period was down 2.4 cents per lb. or 1.9 percent to 126.3 cents per lb. compared to the corresponding week in January 2024. The attached USDA figures denotes average prices over three-years.

Leading QSRs are using increasing quantities of breast meat for sandwiches, strips and nuggets. Inflation is increasing consumer awareness of value with chicken benefitting at the expense of beef and pork

The USDA National benchmark prices in cents per lb. (rounded to nearest cent) are tabulated from the USDA February 223rd Weekly National Chicken Report

|

Product

|

USDA

Feb. 23rd

2023

Cents/lb.

|

USDA

Jan. 19th

2024

Cents/lb.

|

Difference.

%

|

|

Whole

|

127

|

129

|

-1.6

|

|

MSC

|

26

|

26

|

Unchanged

|

|

B/S Breast

|

126

|

118

|

+6.8

|

|

Whole Breasts

|

104

|

102

|

+2.0

|

|

B/S Thighs

|

124

|

106

|

+17.0

|

|

Whole Thighs

|

65

|

62

|

+4.8

|

|

Drumsticks

|

46

|

44

|

+4.5

|

|

Leg Quarters

|

46

|

42

|

+9.5

|

|

Wings (whole)

|

196*

|

171

|

+14.6

|

*Incorporated Super Bowl and play-off weekends

The USDA posted live-weight data for the past week ending January 19th and YTD 2024 were:-

|

Live Weight Range (lbs.)

|

<4.25

|

4.26-6.25

|

6.26-7.25

|

>7.76

|

|

Proportion past week (%)

|

21

|

27

|

23

|

29

|

|

Change from 2020 YTD (%)

|

+16

|

-16

|

-12

|

+9

|

During the week ending February 17th 2024 broilers for QSR and food service (live, 3.6 lb. to 4.3 lb.) represented 16 percent of processed volume compared to 14 percent during the corresponding week in January 2024.

On February 19th 2024 cold storage holdings of processed poultry other than chicken at selected centers amounted to 73,350 lbs. 4.0 percent less than the inventory of 76,386 lbs. on February 1st 2024.

According to the February 26th 2024 USDA Cold Storage Report, issued monthly, stocks of broiler products as of January 31st 2024 compared to January 31st 2023 showed differences with respect to the following categories:-

- Total Chicken category attained 831.6 million lbs. (378,003 metric tons) corresponding to approximately 1.2 weeks production based on recent weekly RTC output. The January 31st 2024 inventory was down 6.5 percent compared to 889.6 million lbs. (404,339 metric tons) on January 31st 2023 and down 5.0 percent from the previous month of December 2023.

- Leg Quarters were down by 19.5 percent to 57.7 million lbs. compared to January 31st 2023 consistent with the data on exports. Inventory was down 13.1 percent from December 31st 2023. Given the trend in inventory of leg quarters it is evident that this category continues to be shipped in varying quantities as the principal (97 percent) chicken export product to a number of nations but with approximately 30 percent of this category comprising shipments to China.

- The Breasts and Breast Meat category was down 2.4 percent from January 31st 2023 to 235.4 million lbs. indicating a relatively stable domestic consumer demand despite concern over inflation in the cost of protein. January 31st 2024 stocks were 3.3 percent lower than on December 31st 2023 suggesting higher retail and food service demand for this category with promotion of chicken sandwiches by QSRs in the face of an increased pattern of eat-at-home consumption.

- Total inventory of dark meat (drumsticks legs, thighs and thigh quarters but excluding leg quarters) increased 37.0 percent from January 31st 2023 to 79.3 million lbs. This decrease suggests a decline in domestic demand for lower-priced dark meat against the prevailing price of white chicken meat.

- Wings showed a 15.7 percent decrease from January 31st 2023, contributing to a stock of 55.4 million lbs. This category was 17.3 percent lower compared to December 31st 2023. Movement in stock over the past 12 months has demonstrated growth in demand for this category. Sales are impacted by competition from “boneless wings.” Increased consumption traditionally associated with significant sports events reduced volume in storage earlier in 2023. The progressive increase in unit price during the first quarter of 2023 should be repeated in 2024.

- The inventory of Paws and Feet was 16.8 percent lower than on December 31st 2023 to 28.6 million lbs. but inventory was 0.6 percent higher than on December 2023. Prior to the April 2020 Phase-1 Trade Agreement approximately half of the shipments of paws and feet destined for Hong Kong were landed and transshipped to the Mainland, a trend that is re-emerging. For 2023, 405,313 metric tons of U.S. broiler products were shipped to China, valued at $711,172 with an average unit value of $1,755 per metric ton. A breakdown of product categories and prices provided by USAPEEC confirmed that Paws and feet represented 68.5 percent of volume and 73.1 percent of value with a unit price of $1,871 per metric ton.

- The Other category comprising 357.0 million lbs. on January 31st 2024 was down 6.3 percent from January 31st 2023 but represented a significant 42.9 percent of inventory. The high proportion in the Other category suggests further classification or re-allocation by USDA to the designated major categories.

January 2024 Production

The USDA Poultry Slaughter Report released on February 22nd 2024 covered January 2024 comprising 23 working days. The following values were documented for the month:-

- A total of 815.3 million broilers were processed in January 2024, up 11.2 million or 1.4 percent from January 2023;

- Total live weight in January 2024 was 5,362 million lbs., up 102.2 million lbs. or 1.9 percent from January 2023;

- Unit live weight in January 2024 was 6.58 lbs., up 0.04 lb. or 0.6 percent from January 2023.

- RTC in January 2024 attained 4,052 million lbs., up 79.8 million lbs. or 2.0 percent from January 2023.

- WOG yield in January 2024 was 75.6 percent, unchanged from January 2024.

- The proportion marketed as chilled in January 2024 comprised 93.1 percent of RTC output.

- Ante-mortem condemnation as a proportion of live weight attained 0.22 percent during January 2024 compared to 0.21 percent in January 2023.

- Post-mortem condemnations as a proportion of processed mass corresponded to 0.48 percent during January 2024 compared to 0.52 percent in January 2023.

Comments

For 2023 exports of broiler parts and feet combined attained a volume of 3,635,178 metric tons (3,794,328 metric tons in 2022) with a value of $4,739 million ($5,217 million in 2022). Unit value decreased 5.2 percent from 2022 to $1,304 per metric ton (including feet) from $1,375 per metric ton.

Mexico has recognized the OIE principle of regionalization after intensive negotiations between SENASICA and U.S. counterpart, the USDA-APHIS assisted by USAPEEC. Provided importing nations adhere to OIE guidelines on regionalization, localized outbreaks of avian influenza and Newcastle disease will affect exports from states with outbreaks in commercial flocks. The response of China, Japan and some other nations is more predictable with bans on a statewide basis. The response by China to outbreaks is influenced more by self-interest than considerations of scientific fact or international trade obligations. Other importing nations have confined restrictions to counties following the WOAH principle of regionalization. The challenge facing exporting nations will be to gain acceptance for controlled vaccination against HPAI in specific sectors and regions with appropriate surveillance and certification to the satisfaction of importing nations.

Collectively our NAFTA/USMCA neighbors imported broiler products to the value of $1,175 million in 2021 and $1,256 million in 2022 compared to 2023 at $1,246 million.

The USDA February projection for RTC broiler production over 2024 will be 46,75 million lbs. with a per capita consumption of 100.1 lbs. Exports amounting to 7,215 million lbs. will represent 15.4 percent of production.

Effective mid-February 2024 the fall 2023 wave of HPAI has resulted in loss of 2.0 million broilers on 8 farms in four states. A total of 130,000 broiler breeders were depopulated on four farms in three states.